Introduction

Artificial intelligence is no longer an experimental capability in insurance. It has become a business-critical engine powering underwriting decisions, claims automation, fraud detection, pricing optimization, customer engagement, and operational efficiency. Yet, as insurers accelerate AI adoption, a larger strategic question is emerging: How can organizations innovate responsibly while controlling risk?

This is where AI Governance in Insurance becomes indispensable.

Insurance is one of the most highly regulated industries in the world. Decisions driven by algorithms can directly affect pricing fairness, claims approvals, customer eligibility, fraud investigations, and compliance obligations. Poorly governed AI models introduce serious risks—bias, lack of explainability, model drift, privacy concerns, regulatory violations, and reputational damage.

For insurers, governance is no longer just a technical requirement. It is an enterprise-wide strategic capability.

According to McKinsey, insurers are expected to derive significant operational value from AI in claims, underwriting, and servicing over the next decade, but only organizations with strong governance foundations will scale AI safely and sustainably.

This blog explores how insurance leaders can build an enterprise-ready AI governance model—covering regulatory readiness, model oversight, generative AI risks, implementation frameworks, and practical operating strategies that reduce exposure while enabling innovation.

TL;DR

- AI Governance in Insurance has become essential as insurers scale AI across underwriting, claims, fraud detection, and customer engagement.

- Regulatory scrutiny is accelerating through frameworks like the NIST AI Risk Management Framework, NAIC principles, EU AI Act, and ISO 42001.

- Insurance organizations must balance innovation with explainability, compliance, fairness, and operational resilience.

- A modern governance strategy combines data governance, model oversight, GenAI controls, monitoring, and human accountability.

- The insurers that operationalize responsible AI today will gain trust, reduce compliance risk, and create long-term competitive advantage.

Why AI Governance in Insurance Has Become a Boardroom Priority

Insurance companies are rapidly moving from isolated AI experimentation toward enterprise-scale implementation. Predictive models influence underwriting decisions. Intelligent automation accelerates claims processing. Generative AI supports customer communication and policy assistance. Fraud detection increasingly relies on machine learning systems.

The result is a dramatic increase in operational dependency on AI.

However, AI introduces a new category of enterprise risk.

Unlike traditional software systems, AI models evolve, learn from changing datasets, and may behave unpredictably under shifting market conditions. A pricing model that performs well today could unintentionally create discriminatory outcomes tomorrow. A claims automation system may reject legitimate claims because of data quality failures. Generative AI applications may produce inaccurate or non-compliant outputs.

For insurance executives, this raises difficult questions:

What happens when AI decisions cannot be explained?

Regulators increasingly expect transparency in automated decision-making. Insurance organizations must demonstrate how pricing, underwriting, or claims decisions are reached.

Opaque “black box” models can create major legal and compliance concerns.

This challenge is especially important in high-impact use cases such as:

- Underwriting recommendations

- Risk classification

- Claims adjudication

- Customer segmentation

- Fraud scoring

Insurers must therefore establish explainability standards, documentation requirements, and human oversight mechanisms.

Why governance matters more than AI adoption

Many insurers initially focused on how fast they could deploy AI.

The more strategic question today is:

How safely can AI scale across the enterprise?

Leading insurers increasingly recognize that governance enables—not slows—innovation.

Organizations with strong governance frameworks benefit from:

- Faster regulatory approvals

- Higher model trustworthiness

- Reduced compliance risk

- Better stakeholder confidence

- Improved customer trust

For enterprises building AI maturity, governance begins with trusted data foundations. Techment’s practical perspective, executive-ready framework to identify and prioritize enterprise AI use cases that actually drive ROI provides useful guidance for improving enterprise data reliability before scaling AI initiatives.

Understanding the Biggest AI Risks Facing Insurance Organizations

The insurance sector faces unique AI governance challenges because algorithmic decisions directly influence financial outcomes and customer experiences.

Without structured governance, AI adoption can amplify operational and regulatory exposure.

Bias and discriminatory outcomes

Insurance regulators closely monitor fairness.

If historical data reflects biased practices, machine learning systems may unintentionally replicate or worsen inequities.

Examples include:

- Disproportionate pricing outcomes

- Geographic discrimination

- Biased risk segmentation

- Claims approval inconsistencies

AI systems must therefore undergo fairness testing and bias monitoring throughout the model lifecycle.

Insurance executives should ask:

Can we explain why a customer received a particular premium or claim decision?

If the answer is unclear, governance gaps likely exist.

Model drift and performance degradation

AI models deteriorate over time.

Economic changes, evolving customer behavior, fraud trends, and new regulatory requirements can weaken predictive performance.

A fraud detection model trained on historical patterns may fail when new fraud behaviors emerge.

Without continuous monitoring, insurers face hidden operational risk.

Strong governance includes:

- Continuous performance monitoring

- Threshold alerts

- Model retraining policies

- Version control

- Independent validation

Generative AI risks in insurance

Generative AI introduces an entirely different risk profile.

Insurance organizations increasingly use large language models for:

- Claims summarization

- Customer support automation

- Policy explanation

- Internal productivity workflows

- Compliance assistance

However, GenAI systems may hallucinate, generate inaccurate recommendations, or expose sensitive information.

Key risks include:

Hallucinations

Generating incorrect policy information.

Compliance failures

Producing advice that violates regulations.

Data leakage

Exposing sensitive customer information.

Prompt injection attacks

Manipulating model behavior.

Organizations deploying GenAI require stronger governance guardrails than traditional machine learning environments.

For enterprises modernizing AI programs, Techment’s insights on Best Practices for Generative AI Implementation in Business provide valuable implementation guidance.

Read our Best Practices for Generative AI Implementation in Business — A Practical Guide for Enterprises

The 3 Core Approaches to AI Governance in Insurance

Insurance companies evaluating governance solutions typically encounter three strategic approaches.

Each offers advantages and trade-offs depending on organizational maturity, compliance exposure, and technology architecture.

Embedded governance through cloud and hyperscaler ecosystems

Major cloud providers increasingly embed governance directly into AI platforms.

Organizations using enterprise ecosystems often benefit from integrated governance capabilities.

Advantages include:

- Simplified deployment

- Native integration

- Reduced operational complexity

- Centralized tooling

For insurers in earlier AI maturity stages, embedded governance often provides sufficient baseline oversight.

However, insurers should evaluate long-term trade-offs.

The vendor lock-in challenge

Integrated ecosystems may optimize governance primarily for platform usage.

This creates strategic concerns:

- Reduced flexibility

- Limited interoperability

- Difficult migration paths

- Inconsistent governance across multi-cloud environments

For insurers operating heterogeneous AI systems, governance fragmentation becomes a major challenge.

Specialized AI governance platforms

Purpose-built governance solutions focus specifically on enterprise risk management and compliance oversight.

These systems generally offer:

- Stronger explainability tools

- Advanced monitoring

- Better audit trails

- Policy enforcement workflows

- Cross-platform governance

This approach is often preferred by large insurers managing diverse AI portfolios.

Organizations with advanced compliance obligations benefit from platform-agnostic oversight.

Strong governance also depends on modern data governance practices.

Organizations exploring scalable AI foundations should first evaluate data quality frameworks for AI readiness and enterprise governance models to reduce implementation risk.

GenAI governance providers

A newer category focuses specifically on generative AI.

These solutions help insurers manage:

- Prompt governance

- Hallucination monitoring

- Output validation

- Data protection

- Responsible content generation

Because generative AI risks evolve rapidly, insurers need adaptive governance rather than static controls.

The strongest governance strategies increasingly combine traditional model oversight with specialized GenAI protections.

Regulatory Pressure Is Reshaping Insurance AI Strategy

The future of insurance AI governance will be heavily influenced by regulation.

Insurance executives can no longer treat governance as optional.

They must proactively align AI programs with evolving standards.

NIST AI Risk Management Framework

The NIST framework provides structured guidance for trustworthy AI.

It emphasizes:

- Accountability

- Reliability

- Transparency

- Safety

- Risk measurement

Many insurers increasingly use NIST as a governance benchmark.

EU AI Act and global implications

The EU AI Act classifies insurance use cases into risk categories.

High-risk systems face stricter compliance obligations.

Even insurers operating outside Europe may be indirectly affected because global compliance standards often converge.

Insurance-specific regulatory expectations

Insurance regulators increasingly focus on:

- Pricing transparency

- Bias prevention

- Consumer protection

- Decision explainability

- Documentation

Organizations unable to explain AI-driven decisions may face compliance scrutiny.

This is why governance should sit at the intersection of technology, legal, compliance, and business operations.

Modern enterprises must align governance with broader AI strategy.

Techment’s Enterprise AI Strategy in 2026 framework offers guidance for aligning governance with long-term enterprise modernization goals.

Enterprise AI Strategy in 2026

7 Critical AI Governance in Insurance Strategies You Must Implement

Successful AI Governance in Insurance requires more than policies and compliance checklists. Leading insurers are operationalizing governance as an enterprise capability—integrating oversight directly into AI development, deployment, monitoring, and business accountability.

Below are seven strategies that separate scalable, trusted AI programs from high-risk experimentation.

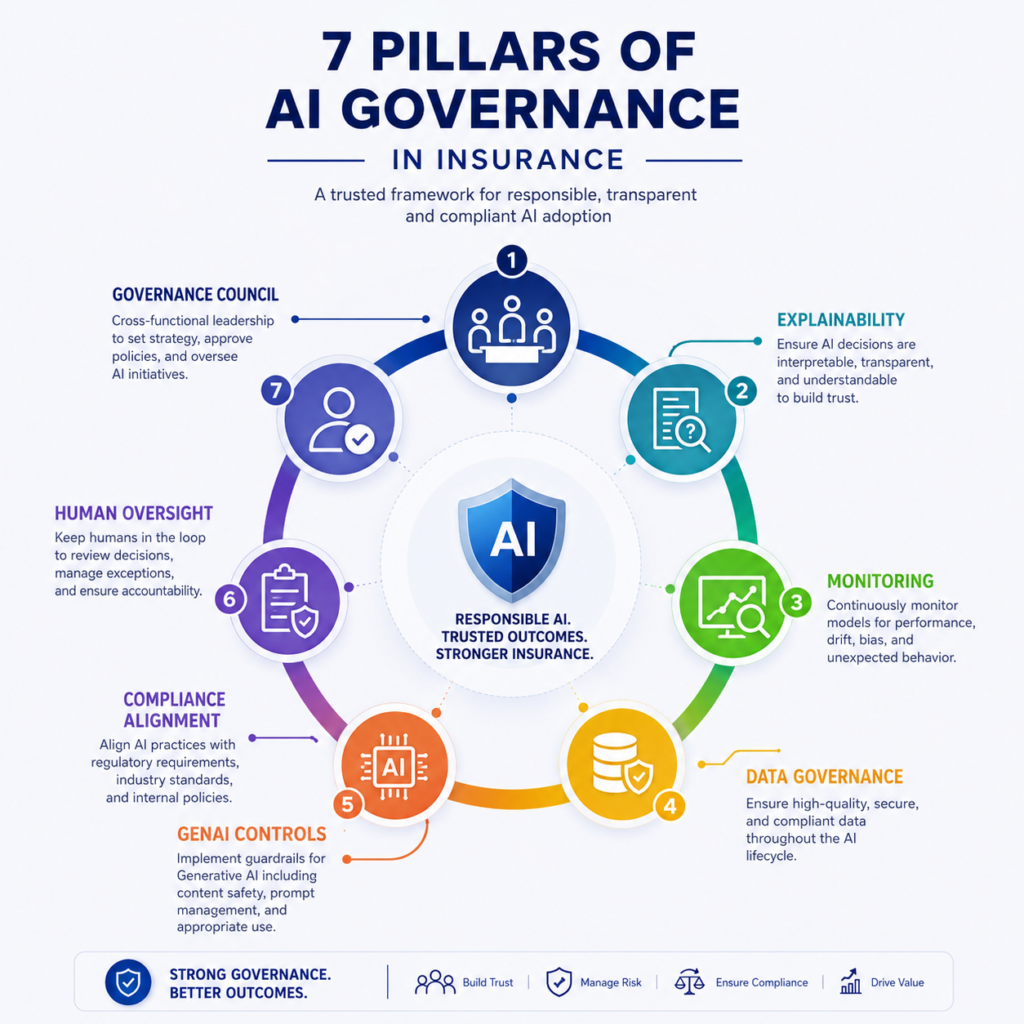

1. Establish an Enterprise-Wide AI Governance Council

AI governance cannot sit exclusively within IT or data science teams.

Insurance organizations require a cross-functional governance structure that brings together:

- Risk leaders

- Compliance teams

- Legal stakeholders

- Data science teams

- Business executives

- Underwriting leadership

- Claims operations leaders

This council should define:

- AI usage standards

- Acceptable risk thresholds

- Governance workflows

- Escalation procedures

- Ethical AI principles

Without enterprise alignment, insurers often face fragmented AI adoption, inconsistent policies, and duplicated governance efforts.

A governance council also helps insurers move from reactive compliance toward proactive risk prevention.

Explore how AI is reshaping insurance across underwriting, claims, risk modeling, customer engagement, and enterprise operations—and what insurers must do to stay competitive in an AI-driven future.

2. Build Explainability into Every High-Impact Model

Insurance decisions affect financial outcomes.

Customers denied coverage or charged higher premiums increasingly expect transparency.

Regulators expect it too.

Explainability frameworks should be mandatory for:

- Underwriting recommendations

- Claims decisions

- Risk scoring

- Fraud classification

- Customer segmentation

Rather than relying solely on black-box systems, insurers should implement interpretable model techniques and explainability layers.

This enables teams to answer:

Why did the model produce this decision?

If insurers cannot confidently answer that question, governance maturity remains incomplete.

3. Introduce Continuous Model Monitoring

Governance should not end once models are deployed.

Insurance environments change constantly.

Economic conditions evolve.

Fraud patterns shift.

Customer behaviors change.

Regulations update.

This creates model drift—one of the largest hidden risks in enterprise AI.

High-performing insurers monitor:

- Accuracy degradation

- Prediction drift

- Data drift

- Bias indicators

- Compliance exceptions

Continuous oversight reduces operational surprises and enables faster intervention before risks escalate.

4. Govern Data Before Governing AI

Poor data quality leads to poor AI outcomes.

Insurance AI systems are only as trustworthy as the data supporting them.

Common issues include:

- Incomplete claims data

- Legacy system inconsistencies

- Duplicate records

- Biased historical data

- Unstructured documentation gaps

Before scaling AI, insurers should prioritize:

- Data lineage

- Metadata governance

- Data quality automation

- Master data consistency

Techment’s guidance on Data Quality for AI in 2026: The Ultimate Blueprint for Accuracy, Trust & Scalable Enterprise Adoption provides useful insight into preparing enterprise data for scalable AI programs.

5. Implement Governance for Generative AI Separately

Traditional machine learning governance is insufficient for GenAI.

Large language models introduce different risks.

Insurance firms deploying AI assistants, policy summarization, claims copilots, or compliance copilots require specialized controls.

Governance priorities include:

Prompt monitoring

Preventing misuse and manipulation.

Hallucination detection

Reducing inaccurate outputs.

PII protection

Avoiding customer data leakage.

Human review checkpoints

Validating sensitive outputs.

Model access controls

Restricting high-risk use cases.

As insurers expand generative AI, governance maturity will increasingly determine scalability.

6. Align Governance to Emerging Regulations

Waiting for regulation to mature is risky.

Forward-looking insurers are proactively aligning governance programs to:

- NIST AI RMF

- ISO 42001

- EU AI Act

- NAIC AI principles

- Responsible AI frameworks

This creates regulatory resilience and reduces future remediation costs.

Organizations that delay governance may face expensive retroactive compliance programs later.

7. Make Human Oversight Non-Negotiable

AI should augment—not replace—critical insurance decisions.

Human oversight remains essential for:

- Claims disputes

- Underwriting exceptions

- High-risk fraud alerts

- Sensitive customer interactions

The strongest insurers implement human-in-the-loop governance, ensuring employees retain accountability for critical outcomes.

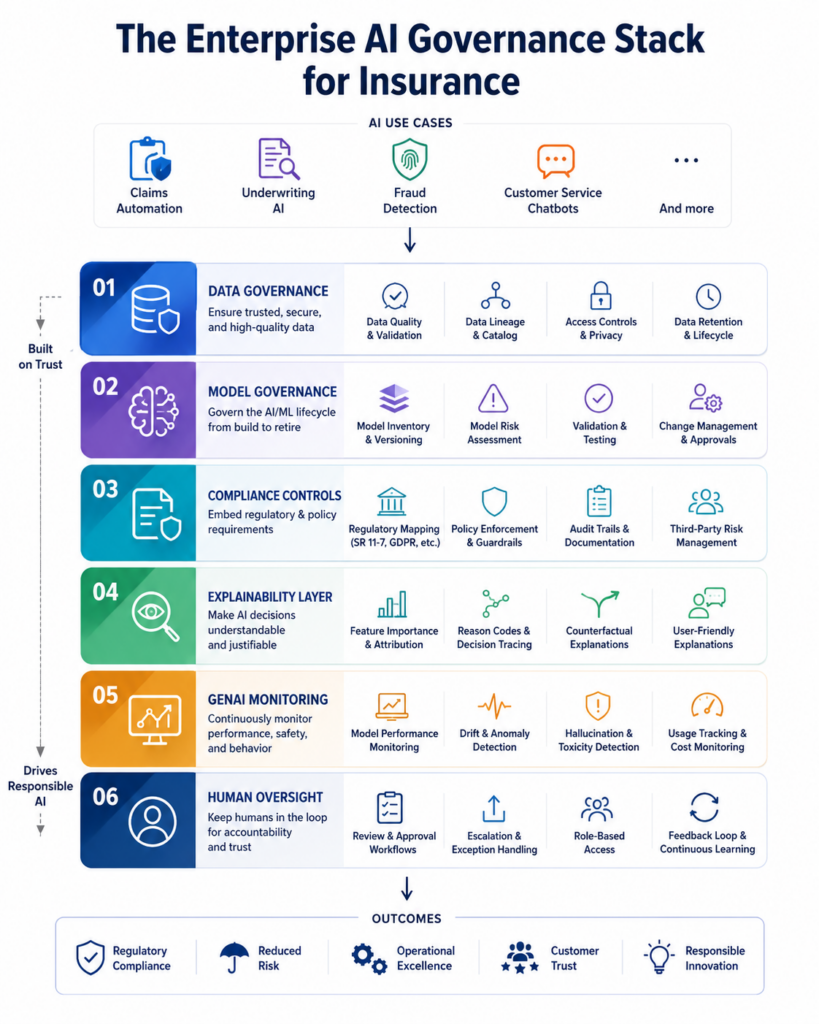

Building an Enterprise AI Governance Framework for Insurance

Governance becomes difficult when organizations treat it as a disconnected control layer.

The most mature insurers instead design governance as an operating model embedded across the AI lifecycle.

The four layers of insurance AI governance

Governance Layer 1: Data Governance

Reliable AI starts with trusted data.

This includes:

- Data cataloging

- Quality standards

- Privacy protections

- Data lineage

- Access controls

Without visibility into data quality, insurers cannot confidently trust AI outputs.

Governance Layer 2: Model Governance

This layer manages:

- Model approvals

- Risk classifications

- Testing standards

- Documentation requirements

- Monitoring frameworks

Every AI model should move through a structured approval lifecycle.

Governance Layer 3: Compliance and Ethics

Insurance organizations must evaluate:

- Bias risk

- Regulatory compliance

- Explainability standards

- Ethical implications

Cross-functional review becomes essential here.

Governance Layer 4: Operational Oversight

Even governed models require continuous accountability.

This includes:

- Drift monitoring

- Audit logs

- Escalation workflows

- Incident management

Strong governance combines automation with business accountability.

Techment’s perspective on Data Governance for Data Quality: Future-Proofing Enterprise Data offers a practical foundation for building enterprise governance maturity.

How to Govern Generative AI in Insurance Without Slowing Innovation

Generative AI is rapidly changing insurance operations.

Customer-facing chatbots now summarize policies.

Claims systems auto-generate documentation.

Internal copilots assist adjusters and underwriters.

But governance complexity increases significantly.

Why GenAI governance is fundamentally different

Traditional predictive models operate within defined statistical boundaries.

Generative AI creates new content.

This introduces unpredictability.

For example:

A claims assistant may generate inaccurate settlement guidance.

A customer chatbot could misinterpret policy language.

A compliance assistant may produce incorrect regulatory advice.

These risks directly affect customer trust and legal exposure.

Key governance controls for insurance GenAI

Leading insurers increasingly implement:

Guardrails for sensitive use cases

High-risk workflows should include:

- Restricted prompts

- Role-based access

- Escalation policies

- Output filtering

Retrieval-Augmented Generation (RAG)

Rather than allowing models to invent responses, insurers increasingly ground outputs in trusted internal knowledge.

This improves:

- Accuracy

- Compliance confidence

- Explainability

Techment’s insights on RAG Models in Enterprise AI offer a practical perspective for reducing hallucination risks while scaling enterprise GenAI adoption.

Human validation layers

Claims approvals, underwriting guidance, and legal communications should never rely solely on autonomous GenAI outputs.

Human checkpoints remain essential.

A Practical Roadmap for Implementing AI Governance in Insurance

Many insurers understand governance importance.

Few know where to start.

A phased approach typically works best.

Phase 1: Assess Current AI Maturity

Evaluate:

- Existing AI systems

- Governance gaps

- Regulatory exposure

- Data readiness

Organizations often underestimate shadow AI usage across departments.

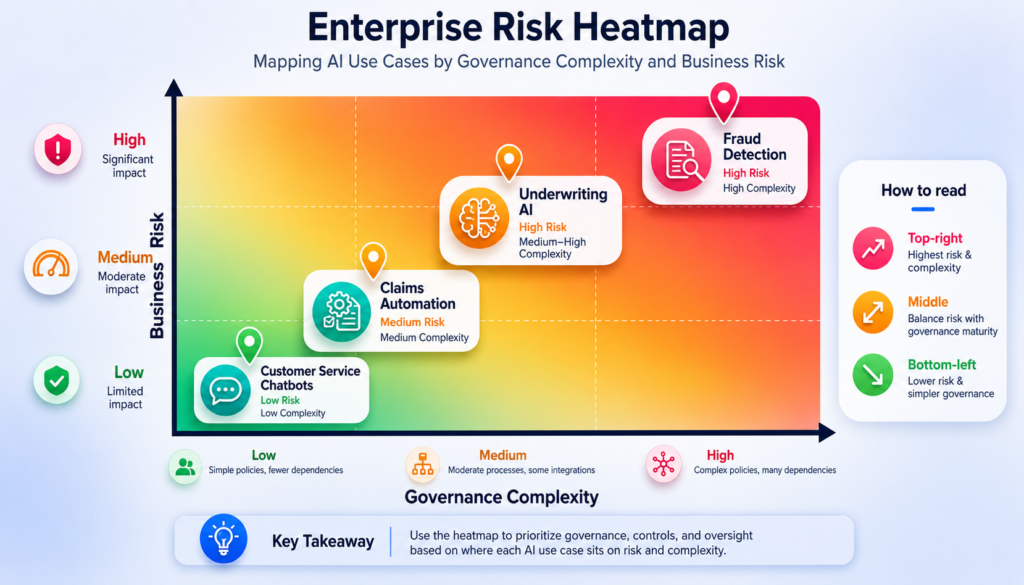

Phase 2: Prioritize High-Risk Use Cases

Focus first on:

- Pricing models

- Underwriting systems

- Claims automation

- Fraud detection

Governance investments should align with business risk.

Phase 3: Define Governance Policies

Establish:

- Approval standards

- Documentation rules

- Risk scoring criteria

- Escalation frameworks

Phase 4: Implement Monitoring Infrastructure

Organizations need:

- Performance dashboards

- Compliance reporting

- Drift detection systems

- Incident workflows

Phase 5: Scale Responsibly

Governance should evolve alongside AI maturity.

Static governance frameworks rarely succeed.

AI systems change rapidly.

Governance must adapt accordingly.

For enterprises scaling AI responsibly, Techment’s Fabric AI Readiness: How to Prepare Your Data for Scalable AI Adoption provides useful guidance.

Fabric AI Readiness: How to Prepare Your Data for Scalable AI Adoption

H2: How Techment Helps Enterprises Build Responsible AI Governance

Insurance organizations face increasing pressure to modernize AI while maintaining trust, transparency, and compliance.

Techment helps enterprises operationalize responsible AI through an end-to-end governance approach that balances innovation with risk management.

Our capabilities include:

Enterprise AI readiness and strategy

Techment helps insurers align AI initiatives with business priorities while creating scalable governance foundations.

This includes:

- AI operating models

- Governance frameworks

- Data readiness assessments

- Responsible AI implementation strategies

Data modernization for trusted AI

Strong governance starts with reliable enterprise data.

Techment supports:

- Data quality modernization

- Enterprise data governance

- Metadata management

- Scalable analytics foundations

Responsible GenAI implementation

Organizations deploying generative AI require stronger safeguards.

Techment helps enterprises establish:

- GenAI guardrails

- RAG-enabled architectures

- Responsible deployment practices

- Compliance-aligned governance

Modern enterprise analytics and AI architecture

Whether insurers are modernizing cloud platforms, preparing for AI at scale, or strengthening governance, Techment supports end-to-end transformation—from roadmap to implementation and optimization.

Conclusion

Artificial intelligence is reshaping the future of insurance.

From underwriting and claims automation to fraud prevention and customer engagement, AI has become a competitive differentiator. Yet innovation without oversight creates unacceptable risk.

This is why AI Governance in Insurance is rapidly becoming a strategic enterprise priority.

Insurers must move beyond fragmented controls toward governance models that combine explainability, compliance, data quality, monitoring, GenAI safeguards, and human accountability.

The organizations that succeed will not necessarily be those adopting AI the fastest—but those governing it the smartest.

As regulations evolve and AI becomes increasingly embedded in business-critical decisions, governance will become a defining capability for resilient insurers.

For enterprises seeking to scale trusted AI responsibly, Techment can help design governance foundations that align innovation with compliance, operational resilience, and long-term business value.

Frequently Asked Questions About AI Governance in Insurance

1. What is AI governance in insurance?

AI Governance in Insurance refers to the frameworks, controls, and policies insurers use to manage AI risk, compliance, fairness, transparency, and operational accountability.

2. Why is AI governance important for insurers?

Insurance organizations face regulatory scrutiny and customer trust risks. Governance helps reduce bias, improve explainability, and ensure responsible AI adoption.

3. How is GenAI governance different from traditional AI governance?

Generative AI introduces risks like hallucinations, prompt injection, and inaccurate content generation, requiring specialized controls beyond traditional model monitoring.

4. Which regulations matter for insurance AI governance?

Key frameworks include:

NIST AI RMF

EU AI Act

ISO 42001

NAIC AI principles

Responsible AI standards

5. What are the biggest AI risks for insurers?

Common risks include:

Bias and discrimination

Model drift

Compliance failures

Lack of explainability

Customer trust issues

Generative AI inaccuracies

Related Reads

- The Future of AI in Insurance: How Intelligent Automation Is Rewiring the Industry

- Data Quality for AI in 2026: The Ultimate Blueprint for Accuracy, Trust & Scalable Enterprise Adoption

- Data Governance for Data Quality: Future-Proofing Enterprise Data

- Best Practices for Generative AI Implementation in Business — A Practical Guide for Enterprises

- Fabric AI Readiness: How to Prepare Your Data for Scalable AI Adoption