Introduction: The Autonomous Shift in Insurance Operations

Insurance has always been workflow-driven.

From underwriting risk assessments to claims adjudication and policy servicing, every function depends on structured processes, compliance controls, and multi-system coordination. Yet these workflows remain fragmented, human-intensive, and increasingly expensive.

Enter AI agents in insurance workflows — not just chatbots or predictive models, but autonomous digital actors capable of perceiving context, reasoning across systems, executing multi-step tasks, and continuously optimizing outcomes.

According to McKinsey, AI-enabled automation could generate up to $1.1 trillion annually across the insurance value chain. Yet most carriers remain stuck at isolated automation pilots rather than full workflow transformation.

The real opportunity is not incremental automation.

It is workflow autonomy — AI agents that:

- Extract claim data

- Validate policy coverage

- Assess fraud probability

- Trigger human review only when needed

- Learn continuously from outcomes

This blog explores how AI agents in insurance workflows transform enterprise operations — architecturally, operationally, and strategically — and what insurance CTOs and CDOs must do to deploy them responsibly at scale.

TL;DR Summary

- AI agents in insurance workflows move beyond chatbots to orchestrate autonomous, multi-step decision processes

- Claims, underwriting, policy servicing, and fraud detection are being redesigned through intelligent automation

- Enterprise insurers adopting AI agents see 30–50% cycle time reduction in operational processes (industry benchmarks)

- Governance, data quality, and operating models determine long-term ROI

- AI agents represent a structural shift from task automation to workflow autonomy

The Market Context: Why Insurance Is Ripe for AI Agents

Insurance is uniquely suited for AI-driven transformation.

It is data-rich, regulation-heavy, process-intensive, and margin-sensitive.

The Economic Pressure

According to Accenture, 40% of insurance operating costs are tied to manual processing and legacy system inefficiencies. Claims leakage, underwriting delays, and fraud misclassification erode margins annually.

At the same time:

- Customer expectations mirror digital-native industries

- Regulatory scrutiny is increasing

- Climate volatility is amplifying risk complexity

- Competition from InsurTech players is accelerating

From Automation to Autonomy

Traditional automation tools (RPA, rule engines) were deterministic.

AI agents introduce:

- Context awareness

- Multi-system reasoning

- Adaptive decision-making

- Continuous learning

This is a structural shift.

Where RPA executes scripts, AI agents orchestrate intent.

For insurers exploring broader modernization, aligning AI agents with an enterprise data strategy is critical — as discussed in Enterprise AI strartegy 2026.

Enterprise Implication

AI agents in insurance workflows are not tactical upgrades.

They are:

- Operational redesign catalysts

- Data architecture accelerators

- Governance stress tests

- Cultural transformation drivers

The question is no longer whether insurers will adopt AI agents.

It is whether they will do so strategically — or incrementally and fragmentedly.

Related Insight: Get a clear, enterprise-grade comparison of agentic vs copilot AI, grounded in process maturity, risk tolerance, and operational readiness.

What Are AI Agents in Insurance Workflows?

AI agents in insurance workflows are autonomous software entities that:

- Perceive data from multiple systems

- Reason using ML models and knowledge graphs

- Execute actions via APIs

- Coordinate with other agents

- Escalate to humans when confidence thresholds drop

Unlike single-model AI deployments, agents are goal-oriented actors.

Core Characteristics

Autonomy

Agents operate independently within policy boundaries.

Contextual Awareness

They synthesize structured and unstructured data — documents, emails, images, policy databases.

Tool Use

Agents can invoke APIs, query databases, trigger payment systems.

Multi-Agent Collaboration

Separate agents can specialize — underwriting agent, fraud agent, compliance agent.

Continuous Learning

Feedback loops refine decisions over time.

Insurance-Specific Capabilities

AI agents in insurance workflows can:

- Read and interpret FNOL documents

- Validate coverage terms

- Estimate claim reserves

- Assess fraud signals

- Generate underwriting summaries

- Monitor regulatory compliance

Related Insights: For enterprise leaders, understanding what is Agentic AI is no longer optional. Read our enterprise guide on Agentic AI and its comprehensive overview.

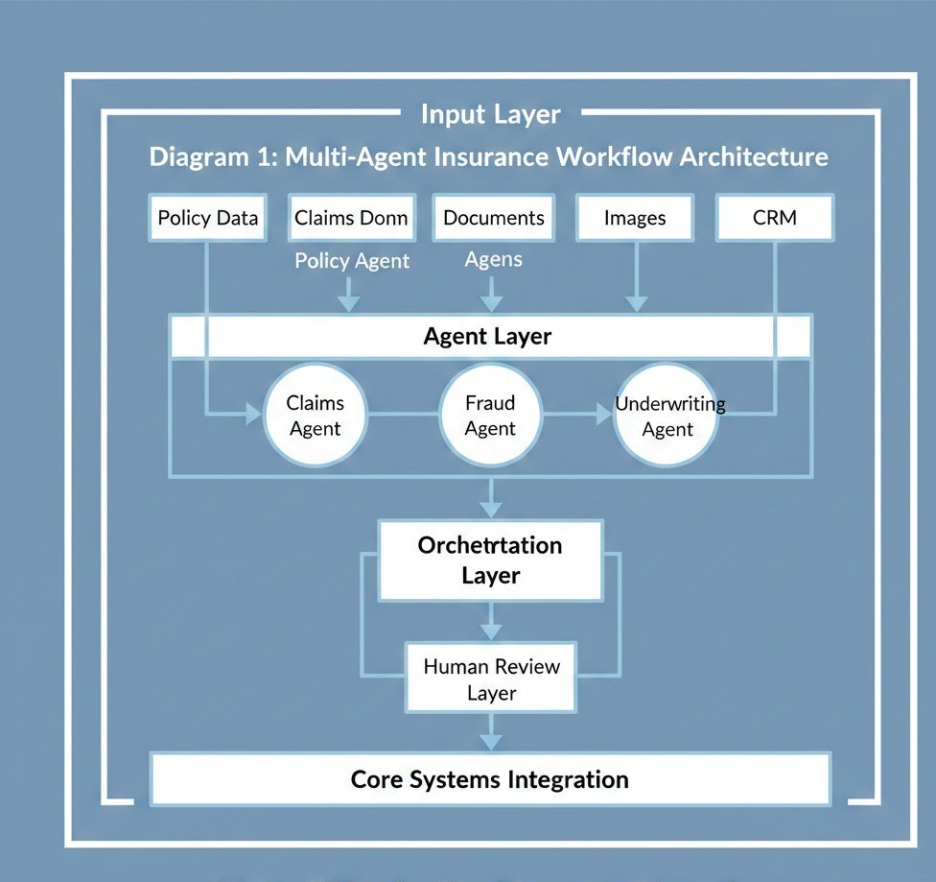

AI Agents in Claims Processing: From FNOL to Settlement

Claims is the most visible application of AI agents in insurance workflows.

It is also the most economically impactful.

Current Challenges

- Manual document review

- High adjudication variability

- Fraud detection lag

- Escalation bottlenecks

- Long settlement cycles

Industry benchmarks show 20–30% of claims require rework due to data inconsistencies.

How AI Agents Transform Claims

An intelligent claims agent can:

- Extract data from FNOL submissions

- Cross-reference policy terms

- Estimate severity using predictive models

- Trigger image analysis for damage assessment

- Score fraud risk

- Recommend payout or escalate

Instead of siloed automation tools, a unified AI agent coordinates all steps.

Business Impact

- 30–50% reduction in cycle time

- Reduced claims leakage

- Higher customer satisfaction

- Lower operational overhead

Governance Implication

Claims decisions impact:

- Regulatory compliance

- Fairness standards

- Brand reputation

Therefore, AI agents in insurance workflows must operate under explainability frameworks and auditable decision trails.

For insurers adopting structured data modernization platforms that enable this orchestration, see Microsoft Fabric Architecture: CTO’s Guide to Modern Analytics & AI

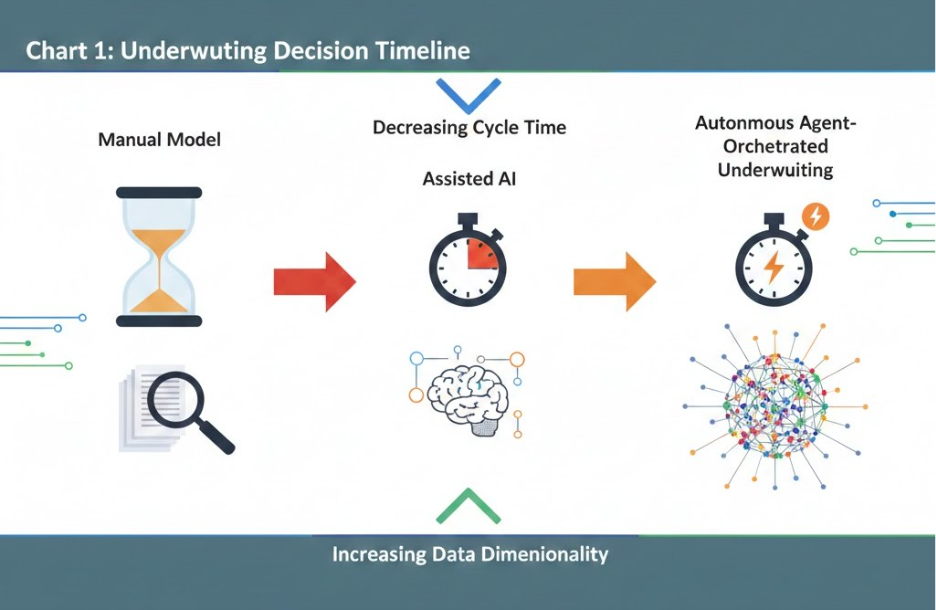

AI-Powered Underwriting: Precision at Scale

Underwriting defines profitability.

AI agents in insurance workflows fundamentally alter underwriting economics.

Traditional Underwriting Constraints

- Manual risk review

- Static risk models

- Delayed third-party data access

- Inconsistent documentation

As risk factors grow more complex — climate exposure, cyber threats, behavioral data — manual underwriting becomes unsustainable.

How AI Agents Enhance Underwriting

An underwriting agent can:

- Aggregate external risk signals

- Generate structured applicant summaries

- Identify anomalies

- Run scenario simulations

- Recommend risk tiers

- Flag compliance exceptions

These agents do not replace underwriters.

They augment decision-making.

Strategic Advantage

Insurers deploying AI agents in underwriting achieve:

- Faster quote turnaround

- More granular pricing

- Reduced adverse selection

- Improved loss ratios

However, model bias becomes a material risk.

AI governance frameworks must evaluate:

- Data representativeness

- Proxy discrimination

- Drift detection

- Regulatory alignment

For insurers aligning underwriting intelligence with governance strategy, see Data Governance for Data Quality: Future-Proofing Enterprise Data.

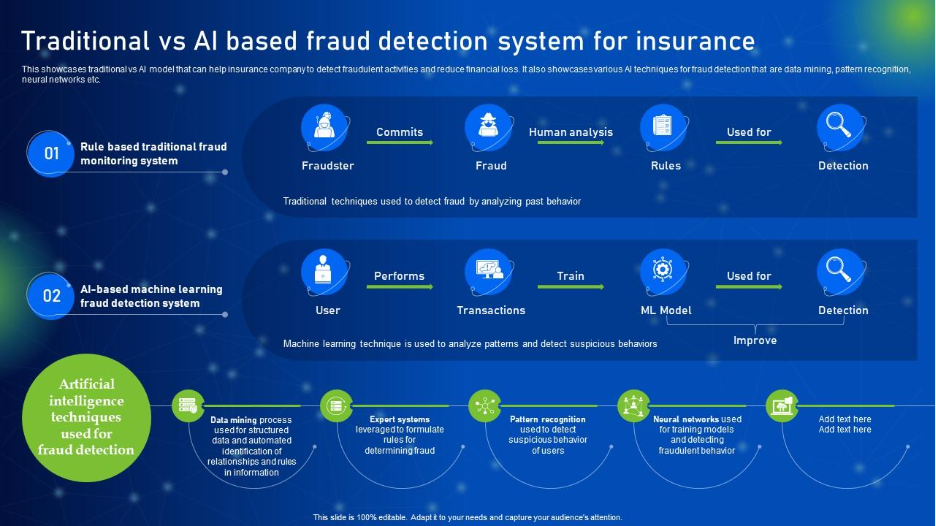

Fraud Detection: Multi-Agent Intelligence Networks

Fraud costs insurers billions annually.

Static rules-based systems cannot keep pace with evolving schemes.

AI agents in insurance workflows introduce network intelligence.

Multi-Agent Fraud Model

- Claim Risk Agent

- Behavioral Pattern Agent

- Social Network Analysis Agent

- External Data Correlation Agent

Each agent specializes but collaborates.

Instead of single fraud scores, insurers gain layered fraud reasoning.

Operational Benefits

- Earlier fraud detection

- Lower false positives

- Reduced investigation workload

- Faster legitimate payouts

However, false positives carry reputational risk.

Enterprise leaders must define:

- Confidence thresholds

- Human override processes

- Bias review mechanisms

For AI-ready data infrastructure enabling such cross-domain intelligence, see AI-Ready Enterprise Checklist for Microsoft Fabric

Customer Experience and Policy Servicing: Conversational to Autonomous

Most insurers began AI with chatbots.

But AI agents in insurance workflows extend beyond conversation.

They:

- Update policy details

- Generate endorsements

- Calculate premium impacts

- Escalate regulatory-sensitive changes

Conversational AI becomes a gateway — not the endpoint.

For a foundational perspective, see Conversational AI for Customer Service: A Step-by-Step Enterprise Guide.

Enterprise Implication

Customer-facing AI agents must integrate with:

- Core policy systems

- CRM platforms

- Billing engines

- Compliance databases

Without unified data architecture, AI agents fragment rather than orchestrate.

Enterprise Architecture Blueprint for AI Agents in Insurance Workflows

Deploying AI agents in insurance workflows requires more than model deployment.

It demands architectural rethinking.

Most insurers operate hybrid environments — legacy core systems, modern APIs, fragmented data lakes, compliance silos. AI agents must operate across this complexity without compromising governance or performance.

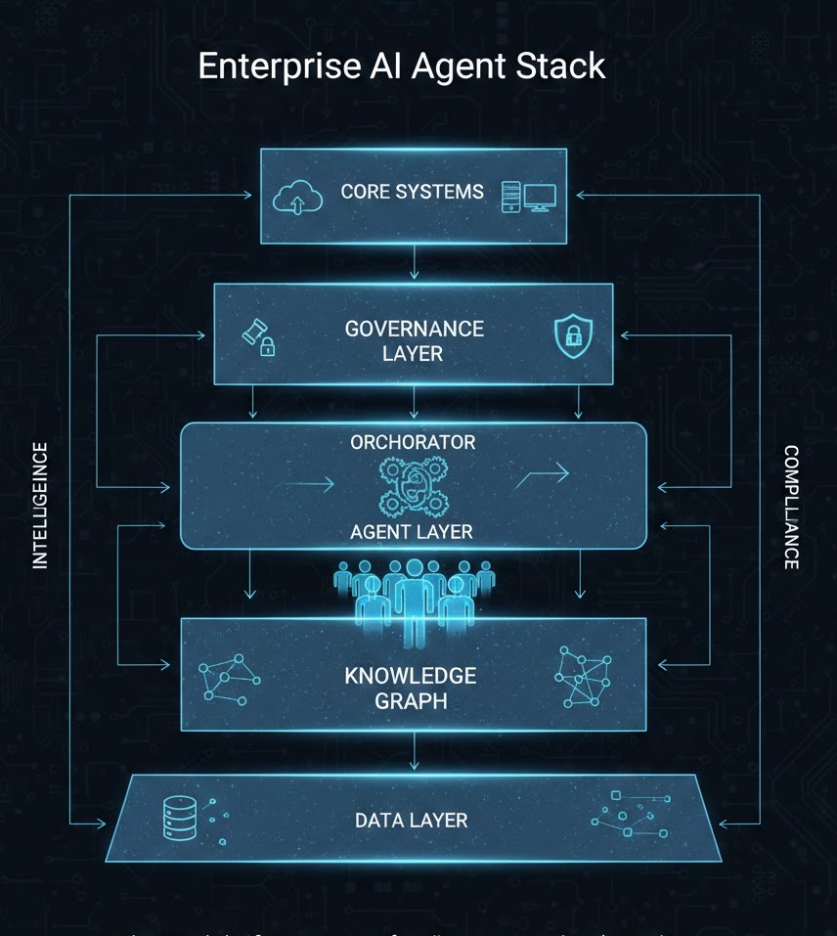

Core Architectural Layers

1. Data Foundation Layer

Unified data access across:

- Policy systems

- Claims platforms

- CRM systems

- External risk databases

- Regulatory repositories

Without trusted data pipelines, AI agents produce inconsistent decisions. A strong foundation aligns with principles outlined in Data Quality For AI.

2. Knowledge & Context Layer

Agents require:

- Policy documentation embeddings

- Regulatory knowledge graphs

- Risk models

- Historical claims memory

This layer transforms raw data into contextual intelligence.

3. Agent Orchestration Layer

A supervisory orchestration engine:

- Coordinates specialized agents

- Applies guardrails

- Tracks decision lineage

- Manages human escalation thresholds

4. Governance & Observability Layer

Includes:

- Decision logging

- Bias monitoring

- Drift detection

- Audit traceability

For insurers exploring modern data platforms that support such orchestration, see What Is Microsoft Fabric? A Comprehensive Overview

Strategic Insight

The architectural decision is not about deploying “an AI agent.”

It is about building an enterprise agent ecosystem.

Operating Model Redesign: From Functional Silos to AI-Enabled Pods

AI agents in insurance workflows disrupt traditional operating structures.

Claims, underwriting, compliance, and fraud teams typically operate independently. But AI agents coordinate across them in real time.

This necessitates new operating models.

The Shift

From:

Functional teams with batch coordination

To:

Cross-functional AI-enabled workflow pods

Each pod includes:

- Domain experts

- AI product owners

- Data engineers

- Risk & compliance oversight

Governance Integration

AI agents require:

- Risk committees reviewing model decisions

- Continuous performance evaluation

- Bias review panels

- Clear accountability matrices

Organizations that fail to align operating models with AI architecture experience:

- Shadow AI usage

- Compliance conflicts

- Model sprawl

- Escalation ambiguity

To align operating model and AI governance maturity, insurers should reference structured enterprise AI roadmaps such as Enterprise AI Strategy in 2026.

Enterprise Implication

AI agents in insurance workflows change how work is defined.

Underwriters shift from data gathering to risk validation. Claims officers shift from processing to exception management.

Leadership must redefine roles before scaling AI agents enterprise-wide.

Risk, Regulation, and Responsible AI in Insurance

Insurance is one of the most regulated industries globally.

Deploying AI agents in insurance workflows introduces compliance complexity.

Key Regulatory Risks

- Algorithmic bias in underwriting

- Unfair claims denials

- Opaque decision logic

- Data privacy violations

- Inadequate auditability

Regulators increasingly demand:

- Explainable AI

- Transparent decision trails

- Human oversight

- Documented risk controls

Governance Mechanisms

Enterprises must implement:

Decision Traceability

Every AI agent action logged and retrievable.

Confidence Threshold Escalation

Automatic human review below defined confidence levels.

Bias & Fairness Audits

Periodic evaluation of demographic impact.

Model Drift Monitoring

Continuous validation of performance against real-world data.

A strong governance backbone aligns with frameworks outlined in Data Governance for Data Quality: Future-Proofing Enterprise Data.

Executive Perspective

Responsible AI is not a legal checkbox.

It is a brand protection strategy.

Insurers deploying AI agents without governance maturity risk reputational damage that outweighs automation gains.

Build vs Buy: Strategic Evaluation for AI Agent Platforms

Insurance leaders face a critical decision:

Should AI agents in insurance workflows be built internally or procured through vendor ecosystems?

Build Advantages

- Full customization

- Data control

- Competitive differentiation

- Tailored regulatory alignment

Build Risks

- High engineering complexity

- Extended deployment cycles

- Talent shortages

- Maintenance overhead

Buy Advantages

- Faster time to market

- Prebuilt compliance templates

- Vendor-supported updates

- Lower upfront complexity

Buy Risks

- Limited customization

- Vendor lock-in

- Integration constraints

- Data portability challenges

The optimal approach is often hybrid:

- Core orchestration layer built internally

- Pre-trained models and infrastructure leveraged via enterprise platforms

For insurers modernizing infrastructure to support hybrid AI strategies, see Microsoft Azure for Enterprises: Cloud AI Modernization

Executive Decision Framework

Evaluate across:

- Data maturity

- Regulatory exposure

- AI talent depth

- Strategic differentiation goals

- Budget horizon

AI agents in insurance workflows must align with enterprise transformation strategy — not operate as isolated innovation experiments.

Implementation Roadmap: Scaling AI Agents Across Insurance Functions

Deploying AI agents in insurance workflows requires phased execution.

Phase 1: Readiness Assessment

Evaluate:

- Data quality maturity

- API accessibility

- Governance framework strength

- Organizational alignment

Reference Fabric AI Readiness: How to Prepare Your Data for Scalable AI Adoption.

Phase 2: Targeted Use Case Pilot

Select:

- High-volume claims process

- Low regulatory sensitivity workflow

- Measurable ROI function

Define success metrics:

- Cycle time reduction

- Escalation rates

- Accuracy thresholds

Phase 3: Multi-Agent Expansion

Add specialized agents:

- Fraud

- Underwriting

- Compliance

- Customer servicing

Integrate orchestration engine.

Phase 4: Enterprise Scaling

- Governance automation

- Cross-functional operating model rollout

- Executive dashboards

- Continuous learning feedback loops

Suggested Chart

Chart 2: AI Agent Maturity Curve

Experimentation → Functional Automation → Cross-Workflow Coordination → Autonomous Enterprise Orchestration

This demonstrates progression for executive stakeholders.

Measuring ROI of AI Agents in Insurance Workflows

Enterprise leaders require quantifiable impact.

Key metrics include:

Operational Metrics

- Claims cycle time

- Quote turnaround time

- Exception rate

- Fraud detection accuracy

Financial Metrics

- Loss ratio improvement

- Operational cost reduction

- Claims leakage reduction

- Premium pricing optimization

Strategic Metrics

- Customer satisfaction (NPS)

- Regulatory incident reduction

- Workforce productivity shift

According to industry benchmarks, insurers deploying advanced AI automation see operational cost reductions of 20–40% across high-volume processes.

However, ROI realization depends on:

- Data integrity

- Governance discipline

- Change management execution

AI agents in insurance workflows amplify existing strengths — and weaknesses.

How Techment Helps Enterprises Implement AI Agents in Insurance Workflows

AI agents in insurance workflows require more than model development.

They demand:

- Data modernization

- Governance design

- Cloud architecture

- AI engineering

- Change management

Techment supports insurers through an end-to-end transformation journey.

1. Data Modernization & AI Readiness

Techment helps enterprises:

- Build unified data platforms

- Modernize legacy insurance systems

- Improve data quality foundations

- Establish AI-ready architectures

2. Intelligent Platform Implementation

Techment designs and deploys:

- Microsoft Fabric-based analytics environments

- Azure AI ecosystems

- Multi-agent orchestration frameworks

- Secure API integrations

See Microsoft Fabric AI Solutions for Enterprise Intelligence

3. Governance & Compliance Frameworks

Insurance AI requires structured oversight.

Techment enables:

- AI governance models

- Data lineage tracking

- Compliance reporting automation

- Responsible AI controls

4. End-to-End Execution

From roadmap to deployment:

- Strategy workshops

- Pilot development

- Enterprise rollout

- Continuous optimization

Techment positions AI agents not as tools — but as enterprise capability accelerators.

Conclusion: From Process Automation to Workflow Autonomy

AI agents in insurance workflows represent a structural transformation.

They move insurers beyond task automation toward autonomous workflow orchestration.

Claims become faster and more consistent. Underwriting becomes more precise. Fraud detection becomes network-intelligent. Customer servicing becomes proactive.

But success depends on:

- Data modernization

- Governance discipline

- Architectural clarity

- Operating model redesign

Insurers that approach AI agents as strategic enterprise capability — rather than tactical automation — will unlock sustainable competitive advantage.

As insurance complexity increases, workflow autonomy will define operational excellence.

Techment partners with insurers to design, implement, and scale AI agents responsibly — ensuring innovation aligns with compliance, performance, and long-term enterprise value.

FAQ: AI Agents in Insurance Workflows

1.Are AI agents replacing insurance professionals?

No. AI agents in insurance workflows augment professionals by automating data-intensive tasks and enabling exception-based decision-making.

2. How long does enterprise deployment take?

Initial pilots can launch in 3–6 months. Enterprise-wide scaling typically spans 12–24 months depending on data maturity.

3. What is the biggest risk in deploying AI agents in insurance workflows?

Insufficient governance and poor data quality pose the highest risks, leading to biased decisions or compliance exposure.

4. Can AI agents operate with legacy insurance systems?

Yes, through API integration layers and orchestration frameworks, though modernization improves scalability and performance.

5. How do insurers ensure explainability?

By implementing decision logging, model interpretability tools, bias monitoring, and structured human oversight checkpoints