Introduction: From Hype to Measurable Enterprise Value

For over a decade, predictions about AI in insurance have oscillated between revolutionary automation and existential disruption. Yet enterprise leaders—CTOs, CDOs, underwriting heads, actuarial leads, and digital transformation executives—are no longer asking whether artificial intelligence will matter. They are asking where it delivers measurable value, how it scales responsibly, and how it reshapes competitive positioning.

Insurance operates on data, probability, and trust. Artificial intelligence enhances all three.

Today’s implementations of AI in insurance are primarily narrow AI models: purpose-built systems trained to solve specific problems such as claims classification, underwriting triage, fraud detection, or pricing optimization. These systems are already reshaping operational efficiency, risk differentiation, and customer experience.

But the strategic opportunity is broader.

AI is not merely automating paperwork. It is enabling insurers to:

- Convert unstructured data into structured intelligence

- Improve risk segmentation and pricing precision

- Reduce fraud leakage

- Accelerate claims payouts

- Expand into parametric and usage-based products

- Improve portfolio steering and capital allocation

The transformation is uneven across the insurance value chain. The winners will be those who integrate AI into enterprise architecture, governance, and operating models—not those who experiment in isolation.

For decision-makers shaping 2026 roadmaps, AI in insurance is no longer optional—it is structural.

TL;DR – Executive Brief

- AI in insurance today is largely narrow AI, delivering measurable ROI in underwriting, claims, and fraud detection.

- The strongest benefits of AI in insurance emerge from augmenting human expertise, not replacing it.

- AI use cases in insurance vary across the value chain, with underwriting triage and claims automation leading ROI.

- Responsible AI governance, data quality, and operating model redesign determine scalability.

- Insurers treating AI as enterprise infrastructure—not experimentation—are building durable competitive advantage.

The Strategic Imperative: Why AI in Insurance Matters Now

Margin Pressure and Risk Complexity

The insurance sector faces mounting structural pressure:

- Climate volatility increasing catastrophic losses

- Inflation driving claims severity

- Fraud becoming more sophisticated

- Customer expectations shifting to instant digital experiences

- Regulatory scrutiny intensifying globally

According to McKinsey, AI-driven automation and analytics could generate substantial economic impact across underwriting and claims functions. Meanwhile, prominent research reports that data-driven decisioning is now a primary competitive differentiator in financial services.

In this environment, the benefits of AI in insurance extend beyond efficiency—they influence loss ratios, pricing competitiveness, and capital efficiency.

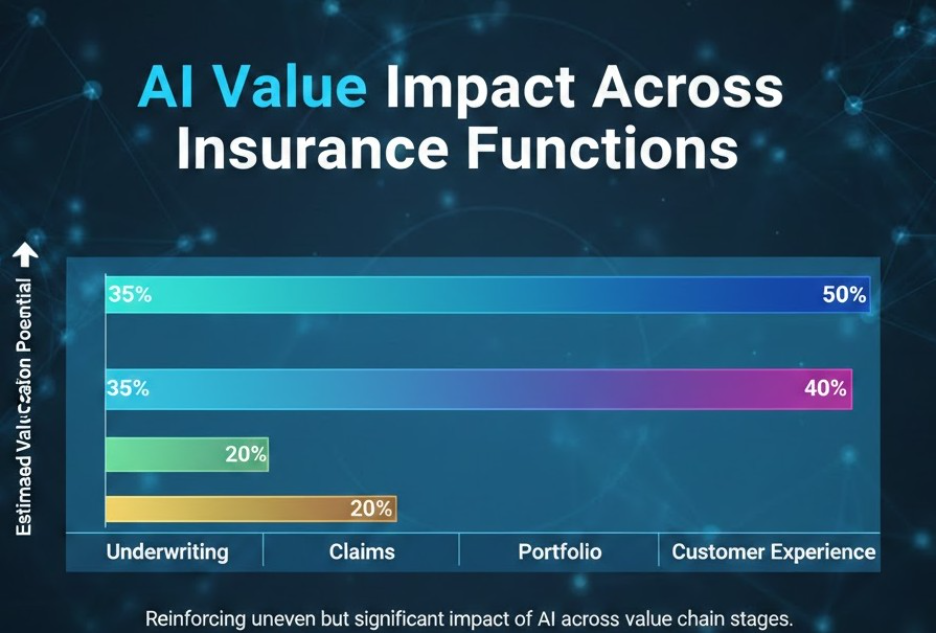

Uneven Impact Across the Value Chain

AI does not affect all insurance processes equally.

Highest impact areas today:

- Underwriting triage and risk scoring

- Claims automation and fraud detection

- Document ingestion via NLP

- Computer vision for damage assessment

- Portfolio risk analytics

Moderate impact areas:

- Distribution optimization

- Customer service automation

- Product personalization

Emerging impact areas:

- Parametric insurance

- Autonomous underwriting ecosystems

- Real-time portfolio steering

Insurers must therefore prioritize AI use cases in insurance based on economic return and data readiness.

Organizations pursuing this journey benefit from structured AI roadmaps such as those outlined in Techment’s Enterprise AI Strategy in 2026.

Narrow AI in Insurance: Understanding the Present Reality

What Is Narrow AI?

AI refers to mathematical models that learn patterns from data and enable automated or accelerated decisions.

Two broad categories exist:

- Narrow AI in insurance: Task-specific models designed for defined outcomes

- General AI: Hypothetical human-level intelligence across domains

Despite media narratives around generative AI, insurance applications remain largely narrow.

Examples include:

- Claims classification models

- Underwriting risk scoring systems

- Fraud anomaly detection engines

- Natural language processing for document ingestion

These systems are bounded, measurable, and auditable.

Why Narrow AI Dominates Insurance

Insurance is a regulated, capital-intensive industry. Decision explainability and model transparency are non-negotiable.

Narrow AI in insurance offers:

- Predictable performance

- Easier compliance validation

- Clear KPIs

- Controlled operational scope

The enterprise lesson: AI value emerges when integrated into workflows alongside human oversight.

As Techment discusses in Data Quality for AI in 2026: The Ultimate Blueprint, scalable AI depends on trusted data foundations.

AI in Insurance Underwriting: Precision, Speed, Differentiation

Data Explosion in Underwriting

Modern underwriting now incorporates:

- Telematics data

- IoT sensors

- Satellite imagery

- Wearables and health data

- Behavioral and transactional data

AI in insurance underwriting converts these diverse datasets into predictive risk scores.

Supervised machine learning models enable:

- Smarter triaging

- Automated document review

- Risk segmentation

- Dynamic pricing adjustments

Business Benefits of AI in Insurance Underwriting

- Reduced turnaround time

- Improved risk differentiation

- Lower adverse selection

- Enhanced customer experience

- Scalable growth without linear cost increases

AI risk assessment in insurance improves portfolio quality when combined with actuarial oversight.

However, risks include:

- Algorithmic bias

- Model drift

- Regulatory challenges

Therefore, governance structures—such as those described in Data Governance for Data Quality: Future-Proofing Enterprise Data—are essential.

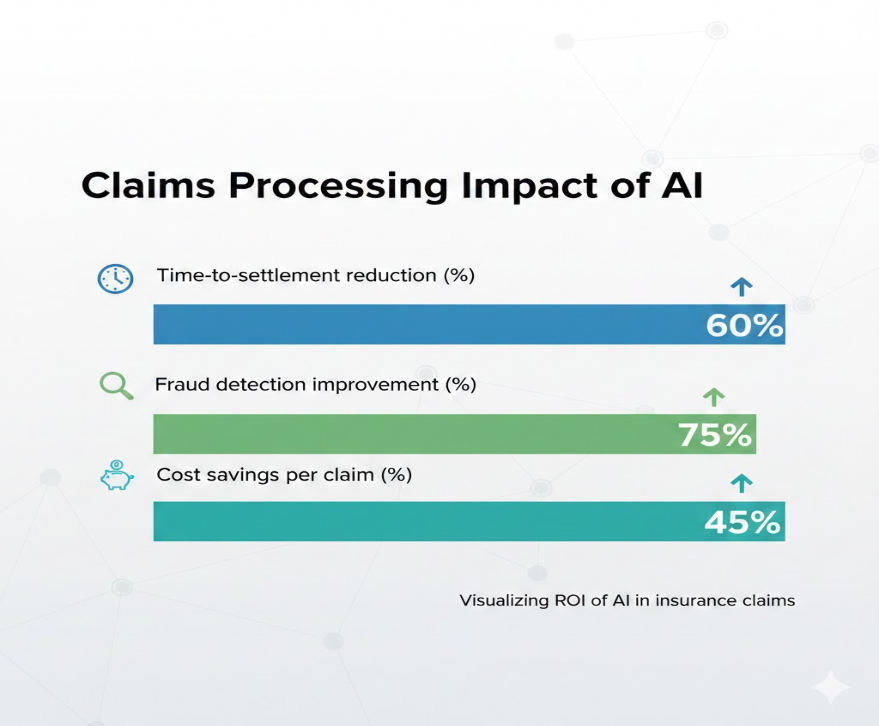

AI in Insurance Claims: Operational Transformation

Claims processing is one of the highest operational cost centers in insurance.

Core AI Use Cases in Insurance Claims

- NLP for document ingestion

- Computer vision for damage assessment

- Fraud detection via anomaly detection

- Predictive severity modeling

- Automated settlement recommendations

The benefits of AI in insurance claims include:

- Faster payouts

- Reduced leakage

- Fraud reduction

- Higher customer satisfaction

Parametric Insurance: Redefining Claims

AI-powered parametric insurance eliminates the traditional claim submission process.

Example scenarios:

- Flight delay compensation

- Weather-triggered crop insurance

- Natural catastrophe coverage

Once predefined parameters are met, payout occurs automatically.

This shifts insurance from reimbursement to real-time response.

Strategic Trade-offs

Benefits:

- Reduced administrative overhead

- Enhanced transparency

- Improved trust

Challenges:

- Trigger accuracy

- Model validation

- Capital implications

- Regulatory scrutiny

AI claims automation must be supported by robust enterprise architecture. Techment’s AI-Ready Enterprise Checklist with Microsoft Fabric outlines readiness considerations.

Computer Vision & Edge AI in Motor Insurance

The convergence of edge computing and AI unlocks new motor insurance capabilities.

Capabilities

- Real-time video capture

- Encrypted cloud transmission

- Computer vision accident reconstruction

- Driving style analysis

- Fraud flagging

AI in insurance motor lines supports usage-based pricing and fraud prevention.

Compliance Considerations

- GDPR data anonymization

- Secure data transmission

- Legal admissibility of AI-derived evidence

This is a prime example of AI use cases in insurance delivering measurable impact while requiring governance maturity.

Portfolio Steering & Risk Intelligence

AI in insurance extends beyond transactional processes into strategic portfolio management.

AI Risk Assessment Insurance Applications

- Exposure aggregation

- Climate risk modeling

- Capital optimization

- Reinsurance structuring

- Catastrophe prediction

Advanced machine learning models allow insurers to simulate portfolio outcomes under various risk scenarios.

Benefits:

- Improved capital allocation

- More resilient portfolios

- Strategic pricing decisions

This represents a shift from reactive underwriting to proactive portfolio intelligence.

Responsible AI in Insurance: Governance as Competitive Advantage

AI adoption at scale introduces new enterprise risks:

- Algorithmic discrimination

- Model opacity

- Cybersecurity vulnerabilities

- Regulatory non-compliance

According to global regulatory trends, explainability is becoming mandatory for automated decisions in financial services.

Core Pillars of Responsible AI in Insurance

- Model transparency

- Human oversight

- Continuous monitoring

- Data lineage tracking

- Bias detection

Responsible AI is not a compliance burden—it is a trust enabler.

Organizations investing early in governance build reputational resilience.

The Operating Model Shift Required for AI in Insurance

AI cannot scale within traditional siloed structures.

Enterprise adoption requires:

- Cross-functional collaboration

- Centralized data platforms

- MLOps capabilities

- Cloud-native infrastructure

- Model lifecycle governance

Insurers that treat AI initiatives as IT experiments struggle to move beyond pilots.

The future belongs to organizations that embed AI into core operations.

Enterprise Implementation Roadmap for AI in Insurance

The strategic promise of AI in insurance becomes tangible only when organizations move from experimentation to structured enterprise execution. Many insurers have dozens of AI pilots—but few have scaled AI across underwriting, claims, and portfolio management in a coordinated manner.

The difference lies in execution maturity.

Phase 1: Data Foundation & AI Readiness

Before scaling AI use cases in insurance, insurers must assess:

- Data quality and completeness

- Availability of historical labeled data

- Governance maturity

- Regulatory alignment

- Cloud and infrastructure scalability

AI risk assessment insurance models are only as reliable as the data that feeds them. Fragmented legacy systems often hinder progress.

A structured modernization journey—such as those outlined in Techment’s Enterprise AI Strategy in 2026 is often the starting point.

Key deliverables in this phase:

- Unified data lakehouse architecture

- Data catalog and lineage mapping

- Master data management

- AI governance framework

- Executive sponsorship and budget alignment

Without these foundations, AI in insurance initiatives remain isolated pilots.

Phase 2: High-Impact Use Case Prioritization

Enterprise leaders should prioritize AI use cases in insurance based on:

- Economic impact (loss ratio improvement, cost reduction)

- Feasibility (data availability, regulatory complexity)

- Strategic differentiation

- Customer experience value

Typical first-wave use cases include:

- Claims triage automation

- Underwriting document classification

- Fraud detection

- Severity prediction

Organizations that attempt to implement advanced generative AI before stabilizing narrow AI in insurance often face governance and trust challenges.

Phase 3: Scalable Architecture & MLOps

To sustain AI in insurance, insurers must establish:

- Model development pipelines

- Version control

- Continuous integration / deployment

- Model monitoring and drift detection

- Retraining workflows

MLOps transforms AI from experimentation into operational infrastructure.

Technology enablers such as cloud-native platforms and integrated analytics ecosystems become essential here. Techment’s AI-Ready Enterprise Checklist with Microsoft Fabric highlights architectural readiness considerations.

Phase 4: Governance & Risk Management Integration

Responsible AI in insurance must be embedded into:

- Compliance review boards

- Model risk committees

- Internal audit processes

- Legal oversight

Governance maturity becomes a competitive differentiator.

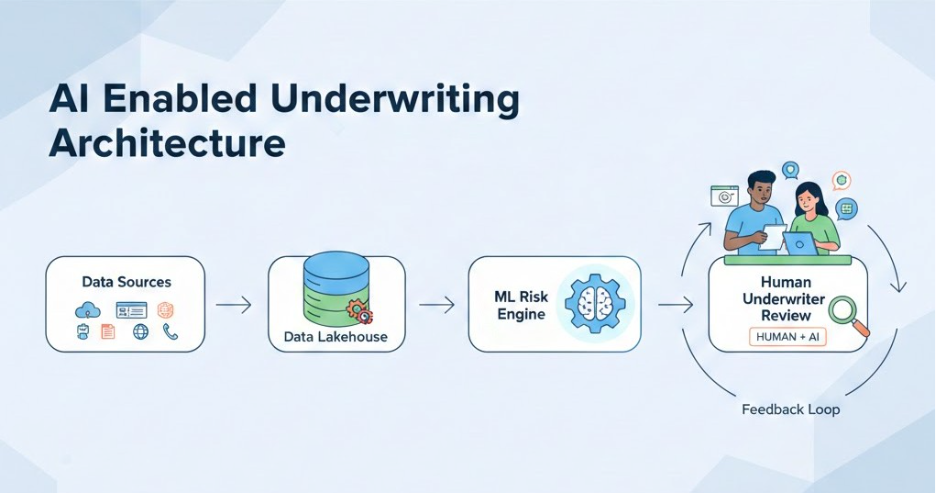

Data Architecture Blueprint for AI in Insurance

AI in insurance depends on unified, governed data architecture.

Core Architectural Components

1. Data Ingestion Layer

Structured and unstructured data sources including:

- Policy systems

- Claims platforms

- Telematics

- IoT sensors

- External weather and satellite data

2. Lakehouse or Unified Data Platform

Central repository for scalable storage and processing.

3. Feature Engineering Layer

Transforms raw data into model-ready features.

4. Model Layer

Machine learning and NLP models trained for specific use cases.

5. Orchestration Layer

Integration into underwriting and claims workflows.

6. Monitoring & Governance Layer

Ensures performance tracking, bias detection, explainability.

Without unified architecture, AI in insurance remains siloed.

Techment’s perspective in Driving Reliable Enterprise Data emphasizes that AI success depends on trusted pipelines.

Benefits of AI in Insurance: Beyond Efficiency

While automation is often the headline benefit, the strategic benefits of AI in insurance are broader.

1. Risk Differentiation Advantage

AI risk assessment insurance models allow granular segmentation. Insurers can price more precisely, reduce cross-subsidization, and enter niche markets confidently.

2. Customer Experience Transformation

AI claims processing insurance shortens settlement cycles from weeks to hours in some cases.

Faster payouts build trust and retention.

3. Fraud Reduction

Machine learning detects subtle anomalies beyond rule-based systems.

Reduced fraud improves combined ratios directly.

4. Operational Scalability

AI augments workforce productivity, allowing insurers to grow without proportional cost expansion.

5. Innovation Enablement

AI-powered parametric insurance products create new revenue streams.

Risks & Trade-offs of AI in Insurance

Enterprise leaders must balance opportunity with risk.

Algorithmic Bias

Biased training data can result in discriminatory underwriting decisions.

Mitigation:

- Bias audits

- Diverse training datasets

- Explainability tools

Model Drift

Risk patterns evolve due to climate, demographics, economic shifts.

Mitigation:

- Continuous monitoring

- Retraining pipelines

Regulatory Scrutiny

Financial services regulators increasingly demand transparency.

Mitigation:

- Model documentation

- Clear decision logs

- Human-in-the-loop processes

Cybersecurity Risks

AI systems introduce new attack vectors.

Mitigation:

- Secure cloud architecture

- Data encryption

- Access controls

Responsible AI in insurance requires structured governance frameworks.

Human + AI: The Augmentation Model

Despite automation narratives, the most successful AI use cases in insurance follow an augmentation model.

AI performs:

- Pattern recognition

- Data processing

- Risk scoring

Humans perform:

- Contextual judgment

- Ethical decision-making

- Exception handling

- Customer relationship management

The future of AI in insurance is collaborative intelligence.

Insurers who remove humans entirely risk reputational and compliance exposure.

Industry Outlook: 2026–2030

The next five years will reshape AI in insurance.

Generative AI Integration

Large language models will enhance:

- Policy document summarization

- Claims communication drafting

- Regulatory report preparation

- Internal knowledge assistants

However, generative AI introduces hallucination risk and governance complexity.

Narrow AI in insurance will remain dominant for core decision-making.

Climate Risk Modeling Acceleration

AI-driven catastrophe modeling will become central as climate volatility increases.

Predictive modeling sophistication will influence reinsurance negotiations and capital reserves.

Embedded & Usage-Based Insurance Growth

Telematics and IoT-enabled AI risk assessment insurance models will support dynamic pricing.

Consumers may accept real-time premium adjustments in exchange for transparency and fairness.

Regulatory Expansion

Expect stronger AI governance mandates across jurisdictions.

Explainability and bias detection capabilities will become mandatory.

Measuring ROI of AI in Insurance

Enterprise leaders must quantify impact.

Key Performance Indicators

Underwriting:

- Quote-to-bind time

- Risk classification accuracy

- Loss ratio improvement

Claims:

- Settlement cycle time

- Fraud detection rate

- Cost per claim

Portfolio:

- Capital efficiency

- Catastrophe exposure modeling accuracy

Customer:

- Net promoter score

- Retention rate

AI in insurance must demonstrate measurable business value—not experimental novelty.

How Techment Helps Enterprises Scale AI in Insurance

Scaling AI in insurance requires:

- Data modernization

- Platform integration

- Governance alignment

- AI lifecycle management

- Change management

Techment partners with insurers to design enterprise AI strategy across:

- Modern data lakehouse architecture

- Microsoft Fabric and Azure AI implementation

- Data governance and compliance frameworks

- AI readiness assessments

- Responsible AI operating models

- End-to-end transformation roadmaps

Techment combines business strategy, architecture expertise, and AI engineering to move insurers from fragmented pilots to enterprise-scale AI ecosystems.

The goal is not isolated AI use cases—but sustainable competitive advantage.

Conclusion: The Strategic Future of AI in Insurance

AI in insurance is no longer a future vision—it is a present capability delivering measurable value across underwriting, claims, fraud detection, and portfolio management.

But the real transformation lies not in automation alone.

It lies in:

- Smarter risk differentiation

- Faster and fairer claims outcomes

- New product innovation

- Stronger governance frameworks

- Scalable enterprise architecture

The insurers who will lead 2026–2030 are those who treat AI as strategic infrastructure—embedded into data, workflows, governance, and culture.

Narrow AI in insurance will continue delivering immediate ROI. Responsible AI in insurance will ensure long-term trust. And enterprise AI strategy will determine competitive positioning.

Techment partners with forward-thinking insurers to design, build, and scale AI ecosystems responsibly—bridging technology capability with business transformation.

The future of insurance will not be purely automated.

It will be intelligently augmented.

Frequently Asked Questions

1. What are the primary benefits of AI in insurance?

The benefits of AI in insurance include improved underwriting accuracy, faster claims processing, fraud reduction, operational efficiency, and enhanced customer experience.

2. Is AI replacing insurance professionals?

No. AI in insurance augments professionals by handling repetitive tasks and providing predictive insights.

3. What is narrow AI in insurance?

Narrow AI in insurance refers to task-specific machine learning models designed for defined use cases such as claims classification or risk scoring.

4. What are the biggest risks of AI in insurance?

Bias, model drift, regulatory non-compliance, cybersecurity vulnerabilities, and poor data quality.

5. How long does it take to implement enterprise AI in insurance?

Typically 12–36 months for full-scale transformation, depending on data maturity and organizational readiness.