Mobile Technology is empowering users to experience Banking without Borders

When speaking about the banking and fintech industry, the first thing that comes to mind is the stand these industries would take in a crisis and pandemic to improve customer service. In this scenario, banks need to respond to the digitalization of industry, mobilization of customers, an influx of competitors, and new regulations, without compromising customer experience. Innovation has always been a driving force behind financial institutions bringing new banking industry trends focused on digital delivery and improved customer experience.

Fintech is the union of financial institutions with technology or technology-enabled financial institutions. The purpose of fintech is to enhance customer experience, productivity, and efficiency of financial institutions with the introduction of mobile platforms, cloud, automation, and smartphones.

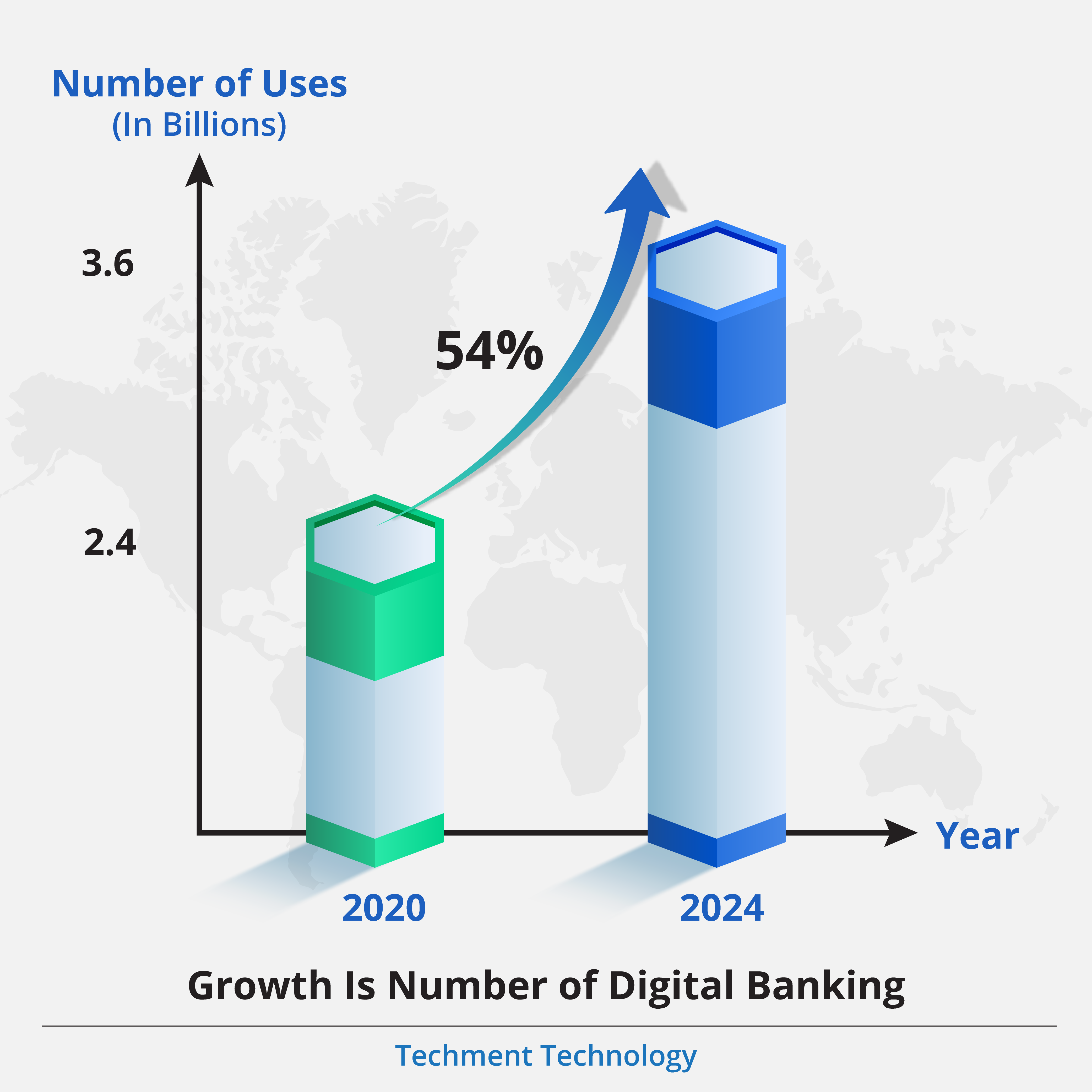

Pandemic commissioned the power of the fintech industry with major areas of changes being security, compliances, ease of remote service, and other functions that have a role in successful digitalization. These factors also fueled the usage of mobile and online banking. This normalized the practices of online deposits, mobile apps, e-payments, etc. According to Juniper Research, digital banking will grow up to 54% i.e., to 3.6 billion by 2024 as compared to 2.4 billion in 2020. To be specific, there has been a 30% increase in mobile banking and 23% rise in online banking worldwide during COVID-19 and will continue to grow in upcoming years, according to BCG (Boston Consulting Group) report.

Factors Fueling the Adoption of Mobile and Online Banking

The mobile revolution in banking was more pushed by fintech companies as they focused on mobile-only operations and emerged as competitors for financial institutions. Mobile banking now has a ubiquitous appeal and has gone mainstream and is popular among people of all age groups.

- More Revenue with Additional Services: Banks and other financial institutions are trying to engage more customers through mobile banking as it brings additional revenue through retail and cross-selling like bancassurance. Online customers often tend to purchase more from banks than branch-only customers.

- Better Communication: With push and in-app notification, mobile banking enhances the customer experience by triggering certain actions and simplifying the solutions. Also, banks convey essential information which has reduced the delay factor and unnecessary movement.

- Enhanced Customer Experience: Mobile banking has highly improved customer experience by building products that add value to them. It facilitated e-deposits, mobile bill payments, and temporary deactivation of credit and debit cards when lost, which were earlier monotonous tasks with traditional banking.

- Increased Operational Efficiency: Mobile banking improves the operational efficiency of banks and the fintech industry by optimizing the information from the fixed central system of the bank. It makes the most accurate and current information available immediately.

During the pandemic, mobile banking became a nifty choice for users. Demand for digital solutions and secure work from home ignited the desire for more ease in banking and financial services pushing the passive financial services and banking trends to flourish.

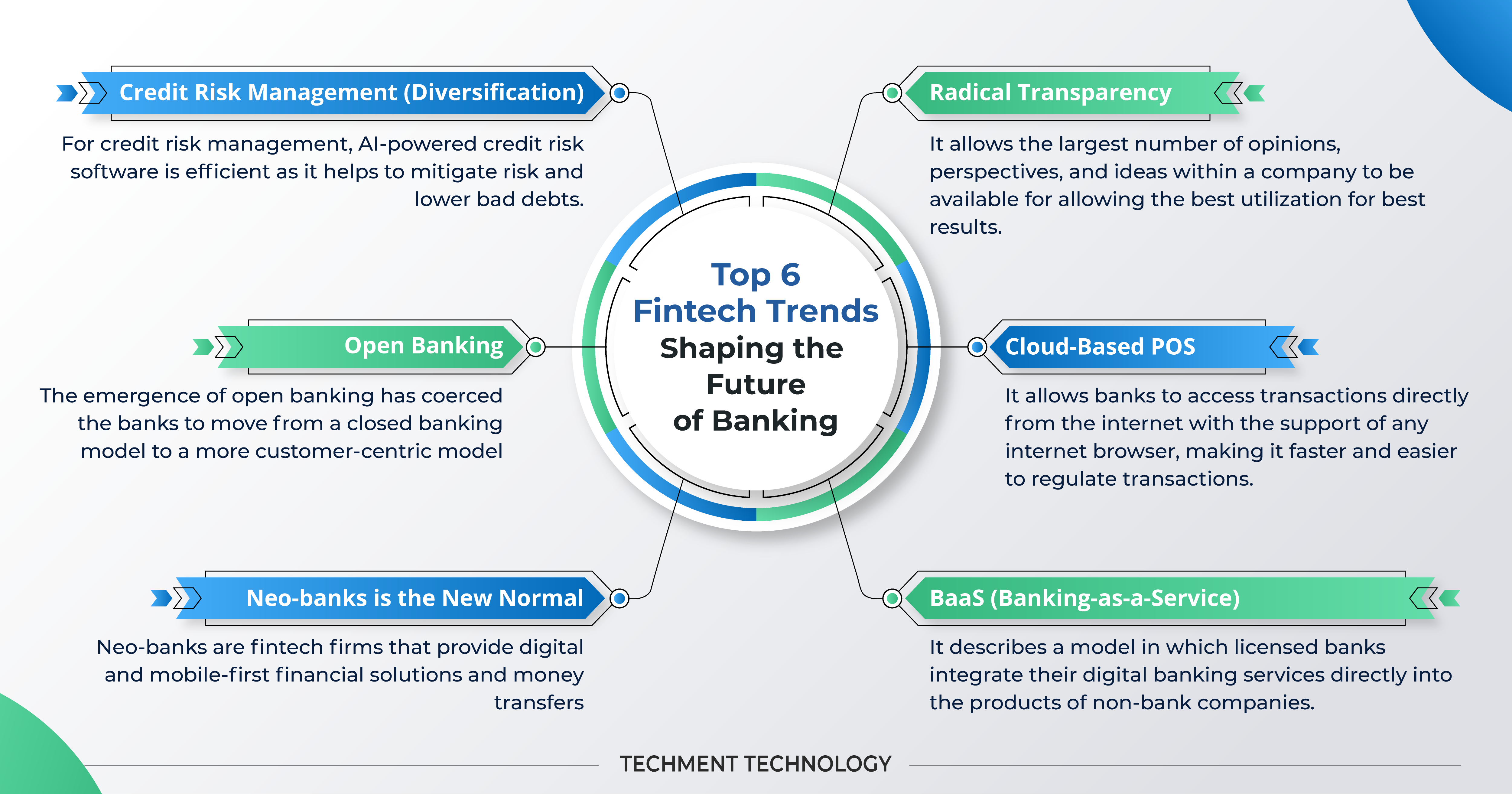

Top 6 Fintech Trends Shaping the Future of Banking

The reach of fintech has become persuasive and is at the forefront because of digital transactions taking place at a higher pace than ever. According to Juniper Research, the global fintech platform revenue is expected to reach $ 638 billion by 2024.

- Neo-banks is the New Normal: Neo-banks are fintech firms that provide digital and mobile-first financial solutions and money transfers and don’t have any physical existence. These are more customer-centric that provide data-driven solutions. The driving features that facilitate the usage of neo-banks are:

- Since neo-banks don’t have a storefront, the account opening is done in a few steps.

- Transactions are seamless and immediate and the details appear immediately on your app which helps customers to report and manage finances in a better way.

Razorpay is the neo-banking platform in India that helps in paying for expenses through corporate cards and paying the vendors of businesses in real-time. According to the 8th edition of the report “The Era of Rising Fintech”, published by Razorpay; the digital transaction in Razorpay increased to 76% in March 2021 as compared to March 2020.

Another popular fintech company, Open is an Indian-origin neobank that offers small businesses and startups with online banking facilities and credit card accounting in a single place. At present, it serves more than 1million businesses and is set to raise $ 100 million, according to Techcrunch. - Radical Transparency: The shift towards remote work for bank employees made it a compulsion to share information in internal networks and was one of the important company strategies. Earlier banks relied on the absolute minimum in terms of sharing information within the network or something between the absolute minimum and everything. But for real business efficiency, the concept of radical transparency had to flourish.

Radical transparency is all about the openness of all information, good or bad. The policy allows the complete information to be accessed by all individuals irrespective of their role and responsibilities. It allows the largest number of opinions, perspectives, and ideas within a company to be available for allowing the best utilization for best results. This makes certain that trust and loyalty are maintained between the company and the workforce. - Credit Risk Management (Diversification): Lending is the key source for banks to retain customers but the risk goes hand-in-hand. Credit risk is simply the risk bank takes while lending money to borrowers, so they need to manage credit risk. Credit risk management is the practice of mitigating losses by understanding a bank’s capital and loan loss reserves at any given time.

For credit risk management, AI-powered credit risk software is efficient as it helps to mitigate risk and lower bad debts. This software collaborates with trusted credit leaders to manage the global portfolio of customers for credit checks, automatically extracts credit ratings, scores, etc. Hence, banks don’t need to toggle between different ERPs to stay alert for credit risk.

DataRobot is an AI-powered platform that allows the preparation of customer data and credit reports. DataRobot was also named as Forbes 2021 Cloud 100 Honoree. - Cloud-Based POS: Point of Sale (POS) is a method of completion of a retail transaction. With the advent of cloud computing, it has become possible to implement a POS system that allows banks to access transactions directly from the internet with the support of any internet browser, making it faster and easier to regulate transactions. They can also be made compatible with various mobile devices such as tablets and smartphones. Some banks have started to create their POS software specifically based on the cloud.

- Open Banking: The emergence of open banking has coerced the banks to move from a closed banking model to a more customer-centric model. Open Banking will facilitate collaboration between financial services partners to support customer requests for the secure exchange of their data with trusted third parties. Services can only be delivered using a cloud-based approach that can adhere to industry standards and interfaces for secure and cost-effective sharing of data with partners.

Open banking is also known as open data banking. Open banking is a banking practice that provides third-party financial service providers with open access to banking services, transactions, and other financial data from banks and financial institutions, through the use of application programming interfaces (APIs). Open banking is emerging as a major source of innovation and is transforming the banking industry. - BaaS (Banking-as-a-Service): BaaS is specifically gaining popularity in retail banking services. It is often seen as an API strategy and is a larger form of open banking. Banking as a Service (or BaaS for short) describes a model in which licensed banks integrate their digital banking services directly into the products of non-bank companies. Thus, a non-banking company, such as an airline, can provide digital banking services to its customers. such as mobile bank accounts, debit cards, loans, and payment services without the need to have your own banking license. The bank’s system communicates via API and connects with the airline’s system, allowing customers to access banking services directly through your airline. It only acts as an intermediary, which means it is not subject to any legal obligations that the bank must meet.

Banks must Leverage Fintech to Transform their Banking and Future

Facing the changing consumer expectations, emerging technologies, and new business models, banks will need to start implementing strategies now to help them prepare for banking in the future. The growing desire of consumers to access financial services through digital channels has led to the proliferation of new banking technologies that are propelling the banking industry.

Collaboration: The digital banking industry could go through a collaborative stage where traditional banks partner with FinTech. As a result, open banking, neo banking, and many other banking models will become increasingly popular. However, some legacy banks may try to build solutions using advanced technologies.

Cloud for better Efficiency: Banks also need to pay more attention to the cloud to improve operational efficiency, scalability and create new banking models. The introduction of the cloud will help banks learn how to handle large and volatile data volumes. Flexibility and long-term growth in the banking sector can open up new revenue streams and mitigate risk through increased capacity, redundancy, and resilience.